As part of our promise to conduct business in as responsible and sustainable fashion as possible, HARMAN has completed a materiality analysis as set forth in the Global Reporting Initiative (GRI) Standards, “Reporting Principles for Defining Report Content.”

Assessing Materiality

In November 2015, HARMAN conducted a refresh of our Materiality Assessment. The assessment sought to confirm material issues identified through a survey of environmental, social and governance (ESG) indicators, evaluate discrepancies between internal and external perception of the importance of various ESG issues, and prioritize what matters most to HARMAN and its stakeholders. The overall Materiality Assessment included a valuation of the information identified as significant during the survey analysis, and the final deliverable was a summary materiality matrix. This assessment was aligned with all GRI G4 Aspects and indicators, and reporting guidelines.

Materiality informs the issues that comprise the focus our corporate responsibility strategy and initiatives and the manner in which we approach related reporting. HARMAN applies the GRI principle that: “Materiality is the principle that determines which relevant topics are sufficiently important that it is essential to report on them. Not all material topics are of equal importance, and the emphasis within a report is expected to reflect their relative priority.”

The GRI defines Material Disclosures as those that reflect the organization’s significant economic, environmental and social impacts; or that substantively influence the assessments and decisions of stakeholders. GRI requires a qualitative analysis, quantitative assessment and discussion to determine if an Aspect is material.

Step 1 – Issue identification

As part of overall corporate responsibility strategy development, a number of interviews and working sessions were completed. Using the GRI G4 Aspects as a starting point, our Sustainability Council began to identify a list of key questions to survey internal and external stakeholders on Aspects that are most material to HARMAN’s business. The internal insights garnered from this effort were supplemented through the ongoing exchange of ideas with key external stakeholders, such as investors (e.g., using CDP and shareholder feedback), customers (e.g., through key questions derived from customer specific data requests), regulatory agencies, nongovernmental organizations, trade associations, partners and community organizations.

Step 2 – Stakeholder survey

To begin the Materiality Assessment process, the HARMAN Sustainability Council identified significant internal and external entities from whom to solicit feedback on material issues from an internal business and external stakeholder perspective. Participants included investors, key customers and HARMAN leadership. Participants in the survey were asked to rank the importance of Aspects in five categories: Business, Environment, Supply Chain, People and Governance. Participants were also asked to provide detailed comments explaining each ranking.

Step 3 – Material Aspect validation

Following the close of the survey collection period, responses were compiled, evaluated and patterned into a materiality analysis. Based on feedback from the Vice President of Corporate Affairs and Communications and the Sustainability Council, HARMAN elected to apply a 20 percent weighting factor to responses submitted by respondents who were also members of the HARMAN Executive Committee. The Executive Committee members play a dual role at HARMAN; they represent the interests of the board and investors as well as HARMAN operations, so their responses to the survey questions received a higher valuation.

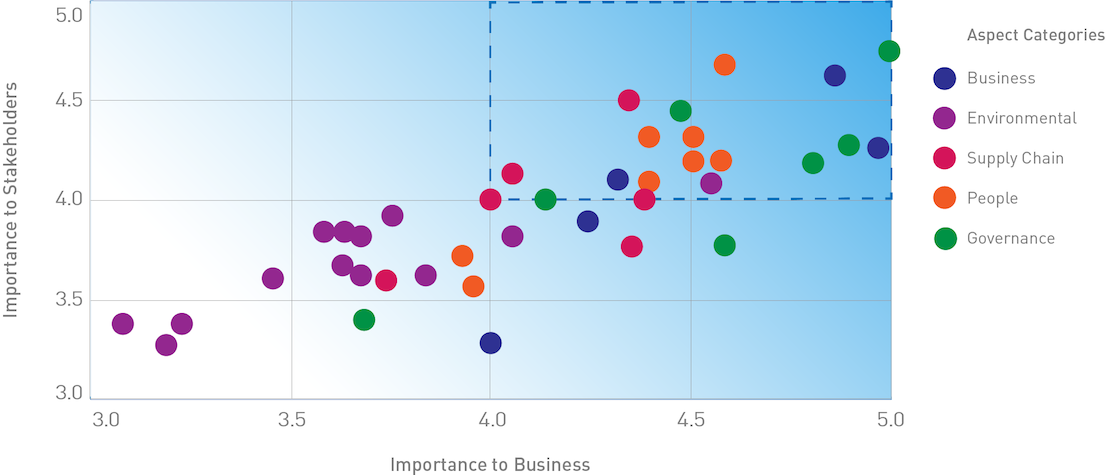

After the weighting was applied to the respective responses, the average internal and external score was calculated for each Aspect. Each Aspect’s average values were plotted on a Materiality Matrix using average internal score (plotted on the x-axis, “importance to business”) and average external score (plotted on the y-axis, “importance to stakeholders”). All Aspects were ranked above a 60 percent average, meaning that all Aspects were considered at least moderately important to HARMAN. Aspects ranking (4,4) or higher were considered “material” to HARMAN.

Step 4 – Review and feedback

The final materiality matrix was presented to the Sustainability Council for review and feedback, and all agreed that HARMAN would proceed with this list of Aspects for the 2016 Sustainability Report. This is HARMAN’s third public sustainability report, which includes all identified material Aspects as well as important additional information to support and celebrate our sustainability story.

Customers Anti-corruption Diversity & Equal Opp. Economic Performance Security Policies & Practices Compliance & Transparency Responsible Sourcing Supplier Environmental Assessment Procurement Practices Market Presence Supplier Human Rights Assessment Workplace exposure risk management Compliance Employee Retention and Recruitment Training, Development, & Education Human Rights Child, Forced, or Compulsory Labor Supplier Assessment for Labor Practices Customer Privacy, External Reporting, Occupational Health & Safety

Customers Anti-corruption Diversity & Equal Opp. Economic Performance Security Policies & Practices Compliance & Transparency Responsible Sourcing Supplier Environmental Assessment Procurement Practices Market Presence Supplier Human Rights Assessment Workplace exposure risk management Compliance Employee Retention and Recruitment Training, Development, & Education Human Rights Child, Forced, or Compulsory Labor Supplier Assessment for Labor Practices Customer Privacy, External Reporting, Occupational Health & Safety